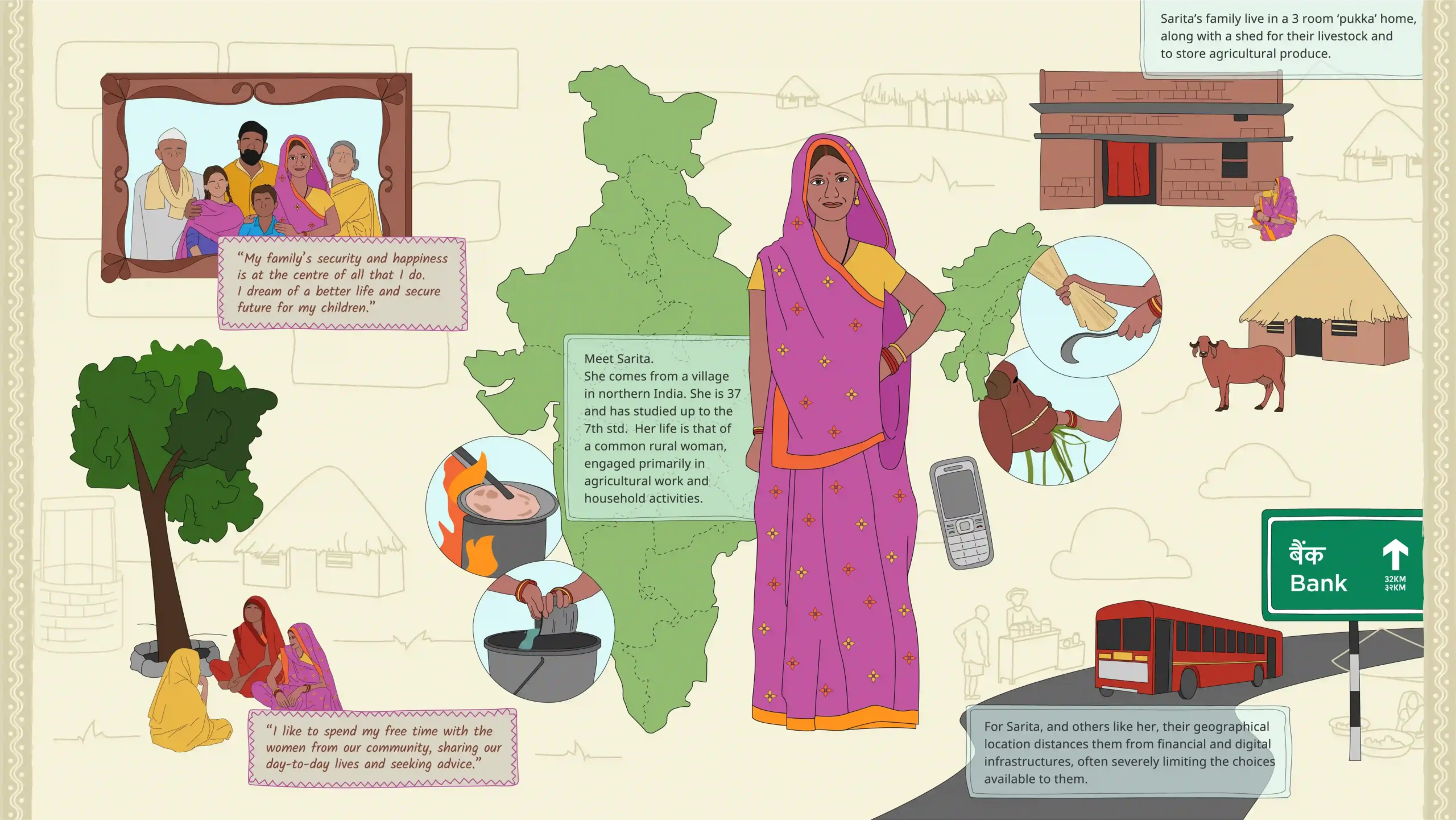

Click on the highlighted states to see where Swadhaar operates across India.

Click on the highlighted states to see where Swadhaar operates across India.